CJ Follini

Publisher

Table of Contents

There’s Still Time For These Year-End Tax Moves

The holiday season brings shopping, bonuses, and—unfortunately—higher taxes. If you earn between $95,000 and $580,000, you’re likely facing tax rates of 25% to 35%, plus capital gains from a strong stock market. But don't worry—there are still ways to reduce your tax burden before year-end.

Here are six strategies we will be discussing today:

Tax-loss harvesting

Charitable donations

Max out retirement accounts

Use your HSA wisely

Itemize deductions instead of taking the standard deduction

Don’t leave FSA money on the table

Let’s dive in!

Make It A Wash: How To Offset Gains With Tax Loss Harvesting

The stock market has been on a tear in 2024, which means some investors have capital gains they have to pay taxes on. Depending on how much you make, the capital gains tax rate for 2024 goes like this:

Tax Rate | Single | Married |

|---|---|---|

0% | $0-44,625 | $0-89,250 |

15% | $44,626 - $492,300 | $89,251 - $553,850 |

20% | $492,300+ | 553,850+ |

Source: Internal Revenue Service

Tax-loss harvesting can help offset these gains. By selling a losing investment, you can reduce taxable gains through a "wash sale / situation"—pairing a winning stock with a losing one. However, there are rules to follow:

Tax-loss harvesting applies only to taxable accounts (stocks, ETFs, etc.), not IRAs or 401(k)s.

You must hold the investment for at least one year.

You can offset up to $3,000 in gains annually.

Be careful: If you break the rules, gains will be taxed as ordinary income.

Who benefits? Individuals in higher tax brackets. The deadline is December 31, so act soon!

Pro Tip: Use your savings from tax loss harvesting to purchase a similar stock, fund or ETF to keep your asset allocation in line.

Source: US Bank

Boost Your Charitable Giving by Year-End

While giving to charity isn’t just about the tax break, it can still pay off. The IRS allows a 60% deduction of your AGI for donations, and if you give long-term assets like stocks or real estate, you avoid paying capital gains tax while deducting the full market value. Just make sure donations are made by year-end and that you itemize deductions on Schedule A of Form 1040.

Who benefits? Those with itemized deductions exceeding the standard deduction ($14,600 for individuals, $29,200 for married couples in 2024).

Pro Tip: Unsure where to donate? Consider a donor-advised fund (DAF), where you get an immediate tax deduction and can direct the funds later.

Max Out Your Retirement Accounts

Get a double whammy for the end of the year by maxing out your tax-deferred retirement accounts like a 401(k) or Traditional IRA. You’ll have more money invested plus it lowers your taxable income. For 2024 you can contribute up to $23,000 in a 401(k). People 50 and over can contribute an additional $7,500. You can contribute a maximum of $7,000, with step-up contributions of $1,000 in an IRA. The deadline for both is December 31.

Who is this for: Anyone who has a tax-deferred retirement savings account who hasn’t maxed out their contributions for 2024.

Pro tip: You don’t have to max it out. Every dollar invested is a dollar less in taxable income.

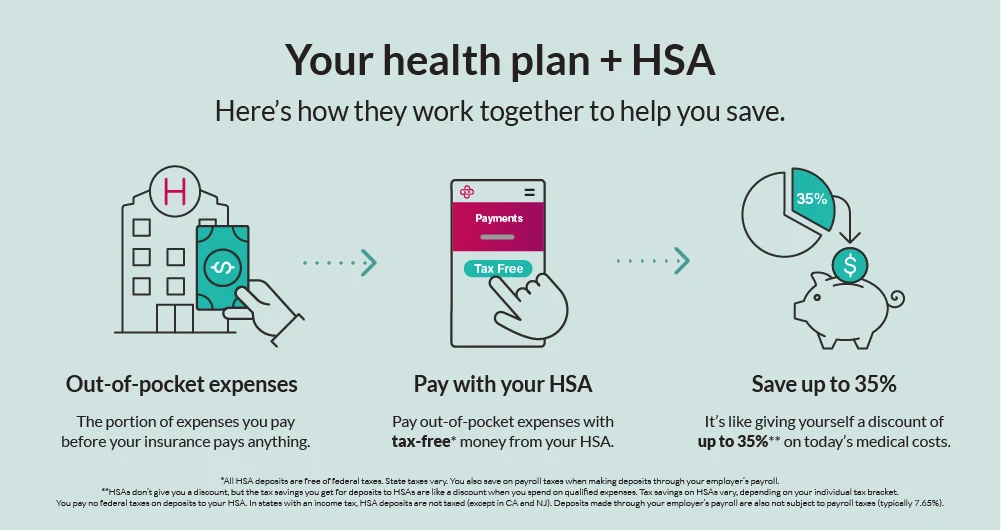

Save More In Your HSA

Health Savings Accounts (HSAs) offer triple tax benefits: contributions reduce taxable income, investments grow tax-free, and withdrawals for qualified medical expenses are tax-free. For 2024, individuals can save up to $4,150, and families can save $8,300. Those 55+ can add an extra $1,000. Don't miss the December 31 deadline to contribute!

Who benefits? Individuals and families with low healthcare costs—more funds mean more growth potential through compounding.

Pro Tip: Use your HSA as a tax-free retirement strategy. It rolls over year after year, helping cover future medical expenses when you retire.

Give Itemizing a Try

The standard deduction is simple—$14,600 for individuals and $29,200 for couples—but itemizing could save you more if your deductions exceed those amounts. You can write off expenses like medical bills, charitable donations, mortgage interest, and education costs.

Who benefits? If your deductions surpass the standard deduction, itemizing is worth it.

Pro Tip: Save your receipts! They’re crucial if the IRS questions your deductions. Just be mindful— not everything is deductible.

Don’t forget your Flexible Spending Account

FSAs let you contribute pretax dollars for medical expenses, which lowers your taxable income. You can contribute up to $3,200 in a FSA for 2024. There’s a catch. If you don’t use it you lose it by year end.. Some plans give you a 2.5 month grace period while others let you carry over $660 per year.

Who is this for: Anybody who hasn’t maxed out contributions for the year and have the grace period or have medical expenses for the remainder of December.

Pro tip: You can use the money on your spouse, children or qualifying relatives.

The Final Word

Taxes are one of life’s certainties but that doesn’t mean you can’t mitigate some of your exposure. These six tax strategies are tried and tested and can ensure you pay less come tax time.