CJ Follini, Publisher

Good morning, Noyackers!

What Does It Mean to Be Wealthy?

For centuries, wealth was about ownership—land, gold, stocks. It symbolized security, power, and legacy. But wealth has never been just about money. The word itself comes from Old English weal, meaning well-being.

Today, the definition is shifting again.

Boomers saw wealth as stability—a pension, a home, a job for life. Millennials, however, see wealth as freedom—control over time, choices, and values.

The old financial system wasn’t built for a generation facing crippling student debt, skyrocketing housing costs, and career instability. Millennials aren’t playing by the old rules—they’re rewriting them.

POLL: What’s the Biggest Roadblock Between You and Financial Freedom?

The Wealth Shift: Why High Earners Stay Broke

My mother used to remind my father (often and loudly) that "it's not what you earn; it's what you keep." That wisdom has stuck with me.

Making more money doesn’t mean building wealth. Without a plan, income disappears as fast as it arrives.

Lifestyle Inflation: A raise comes, and suddenly there’s a new car or bigger apartment. More income, but no wealth.

High-Interest Debt: A little extra spending turns into credit card debt. Interest snowballs, eating away at savings.

Investment Paralysis: Too many options = doing nothing. Fear of mistakes leads to missed opportunities.

📌 Lesson: Hard work alone isn’t enough. Money needs a system. Otherwise, it comes in one door and goes right out the other.

The Rise of DIY Wealth Management

For decades, wealth management meant handing your money to an advisor and trusting the system. But Millennials saw that system fail—market crashes, layoffs, and rising debt made traditional financial advice feel outdated.

Now, they’re taking a DIY approach—and that means:

Investing beyond the stock market—real estate, fine art, venture capital, and alternative assets aren’t just for the ultra-rich anymore.

Optimizing taxes like a business owner—keeping more of what you earn is just as powerful as making more.

Building multiple income streams—rental properties, side hustles, dividends, and digital entrepreneurship.

📌 Lesson: Wealth isn’t just a number in a bank account—it’s about freedom, control, and financial resilience.

Try the AI Personal Wealth Copilot now at WeAreNoyack.com and start optimizing your money like a pro.

How to Build Personal Wealth (Without Relying on Wall Street)

1. Budget Like an Investor, Not Just a Spender

A good salary means nothing if you don’t allocate it strategically. The 50/30/20 Rule is a simple framework:

50% Needs (housing, food, insurance)

30% Wants (travel, entertainment, lifestyle upgrades)

20% Wealth-Building (investments, savings, debt payoff)

🚀 Pro Tip: Before spending on “wants,” allocate your 20% to wealth-building first.

How to Build Personal Wealth (Without Relying on Wall Street)

1. Budget Like an Investor, Not Just a Spender

A good salary means nothing if you don’t allocate it strategically. The 50/30/20 Rule keeps it simple:

50% Needs (housing, food, insurance)

30% Wants (travel, lifestyle upgrades)

20% Wealth-Building (investments, savings, debt payoff)

📌 Pro Tip: Pay yourself first—invest before you spend.

2. Invest Early, Often, and Intelligently

Inflation erodes cash—investing builds wealth.

Even small contributions compound over time.

The Power of Compounding: If you invest $500/month at 8% returns starting at 25, you’ll have $1.5 million by 65. Wait until 35? Less than half that.

Diversification, diversification, diversification…

Fine Art & Collectibles – Alternative assets with long-term appreciation.

Real Estate Syndications – Passive income & equity growth.

Venture Capital – High-risk, high-reward investments in startups.

Index Funds & ETFs – Low-cost, long-term market growth.

📌 Pro Tip: Automate investing—treat it like a subscription, not an afterthought.

3. Use Debt as a Tool, Not a Trap

Not all debt is bad. The key is knowing which debt builds wealth and which destroys it.

Bad Debt: Credit cards, car loans, high-interest personal loans.

Good Debt: Mortgages (for smart investments), student loans (if ROI is strong), business loans (to generate income).

Debt payoff strategies:

Avalanche Method – Pay highest interest first to save the most money.

Snowball Method – Pay smallest debts first for motivation.

4. Pay Less in Taxes, Keep More of Your Wealth

Taxes are your biggest expense if you’re not careful. Smart tax strategies = more money working for you, not the IRS.

401(k)/IRA – Pre-tax contributions lower taxable income.

Roth IRA – Pay taxes now, withdraw tax-free later.

Health Savings Accounts (HSAs) – Triple tax benefits for medical expenses.

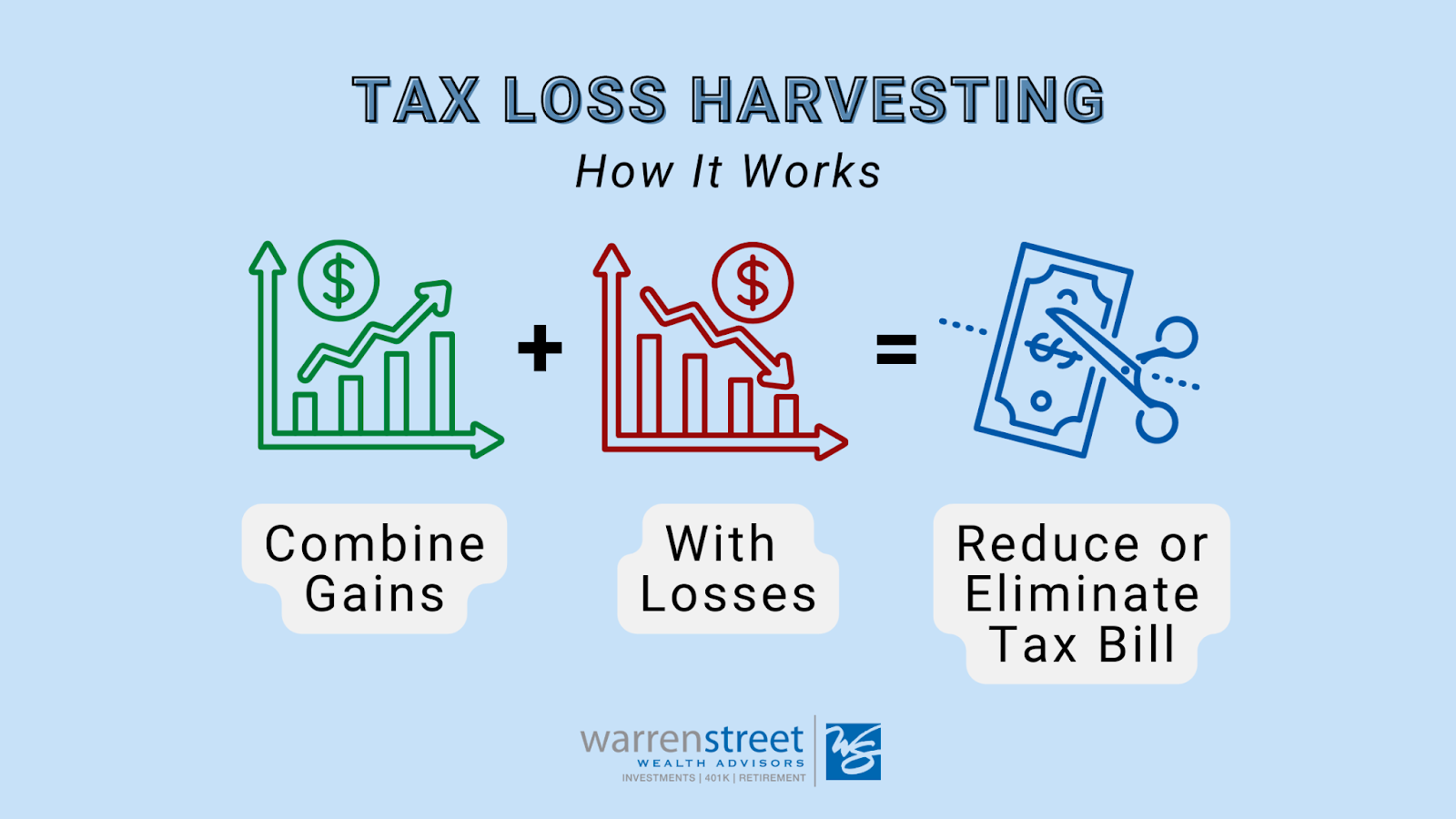

📌 Bonus Tip: Offset gains with tax-loss harvesting—pairing winners with losing stocks to create a wash and lower tax liability.

Final Thoughts: Wealth Is a Choice

Your financial future doesn’t happen by accident. Every decision—where you invest, how you manage risk, how you build income streams—shapes the life you’ll live tomorrow.

The system wasn’t built for Millennials. So they’re building their own.