CJ Follini, Publisher

Good Morning, Noyackers!

Whether you’ve just scored your first job post-grad, or are making a career transition, navigating your paychecks can be stressful and confusing.

In this week's newsletter, we’re going to break down everything you need to know. From how your salary should break down per pay period to what benefits and deductions you should expect to see coming out - by the end, you’ll feel confident reading your pay stubs and understanding where your salary is going - the first step to smarter money management. Don’t forget to share your thoughts in our quick poll at the end - we want to hear from you!

“Don’t work for money; make it work for you.” – Robert Kiyosaki

📊 Poll: How Are You Optimizing Your Paycheck?

💰 The Tax Breakdown: Know What’s Coming Out

Taxes can feel like they’re swallowing up your paycheck, but they’re not as mysterious as they seem.

Federal Income Tax: The amount withheld is based on your Form W-4. Too much withheld? You’re giving Uncle Sam a free loan. Too little? You might owe money come tax time. Use this IRS Witholding calculator to fine-tune your withholdings.

FICA Contributions: These deductions—6.2% for Social Security and 1.45% for Medicare—fund your future benefits. They’re fixed, so you don’t have to worry about adjusting them.

State and Local Taxes: These vary widely depending on where you live. Residents of states with no income tax (hello, Texas and Florida!) have more take-home pay, while those in higher-tax areas can offset costs by maximizing pre-tax benefits like HSAs or 401(k)s.

Deductions: From health insurance to garnishments, there are so many different deductions that can be legally withheld from your pay depending on your individual situation. Here are a few of the most common payroll deductions you can likely expect to see:

Insurance: Employer-sponsored health or life insurance policies are a very common payroll deduction for those seeking health care from their job.

Retirement Contributions: Company-based 401(k) plans, Roth/Traditional IRAS, etc.

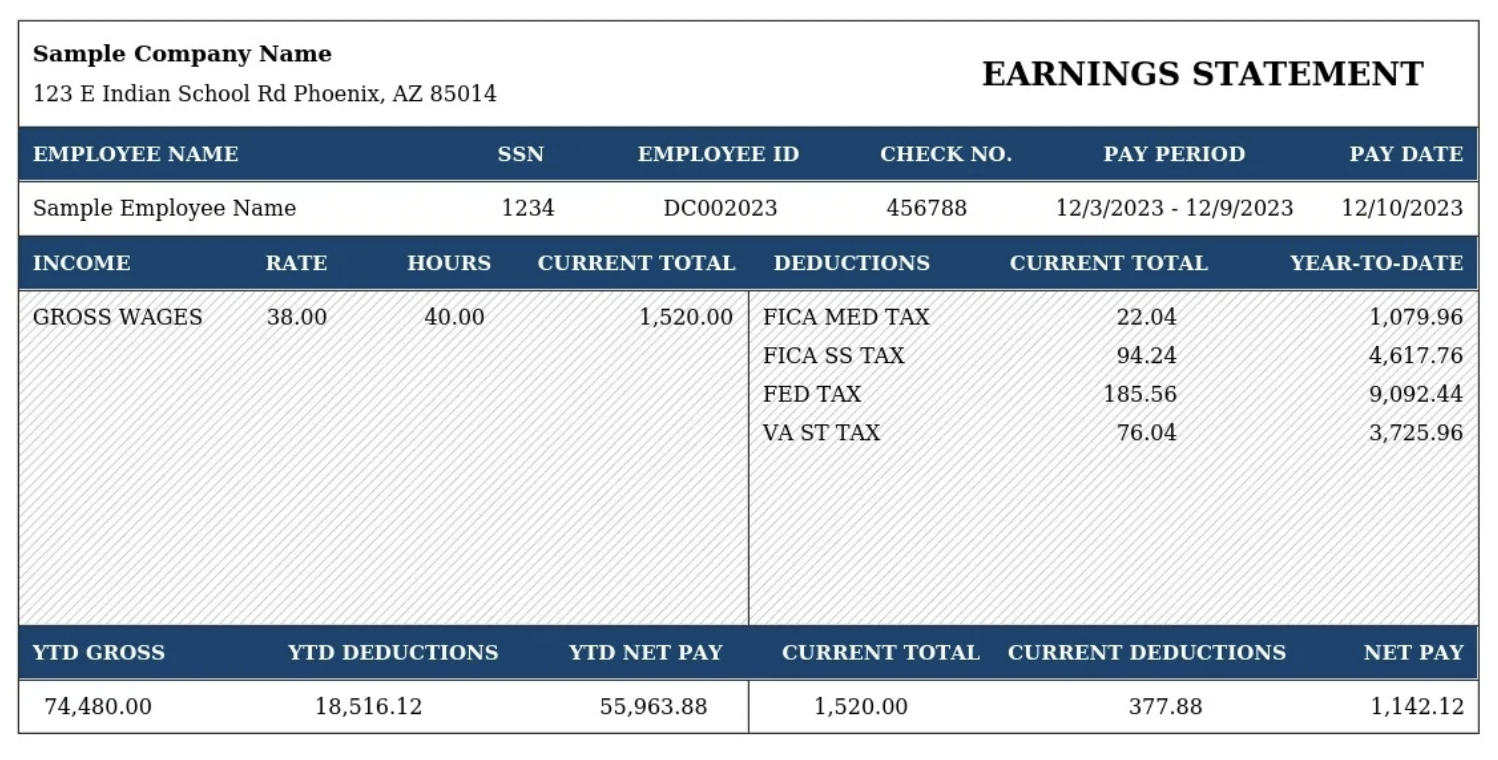

Source: Pay Stubs

🌱 Building Wealth: Think Beyond the Paycheck

Your paycheck isn’t just for today—it’s a tool for creating the future you want.

Maximize Employer Contributions: Always contribute enough to your 401(k) to get the full employer match. It’s like turning down a bonus if you don’t.

Leverage Tax-Advantaged Accounts: HSAs and FSAs (Flexible Spending Accounts) are great for saving on medical and dependent care costs. Just remember, FSAs are “use it or lose it.”

Master Your Budget: Establishing a realistic budget based on your earnings and expenses will go a long way in working towards accomplishing your goals. Consider a simple budgeting method, like the 50/30/20 rule - 50% of your earnings goes towards needs, 30% towards wants, and 20% towards paying off debt and savings.

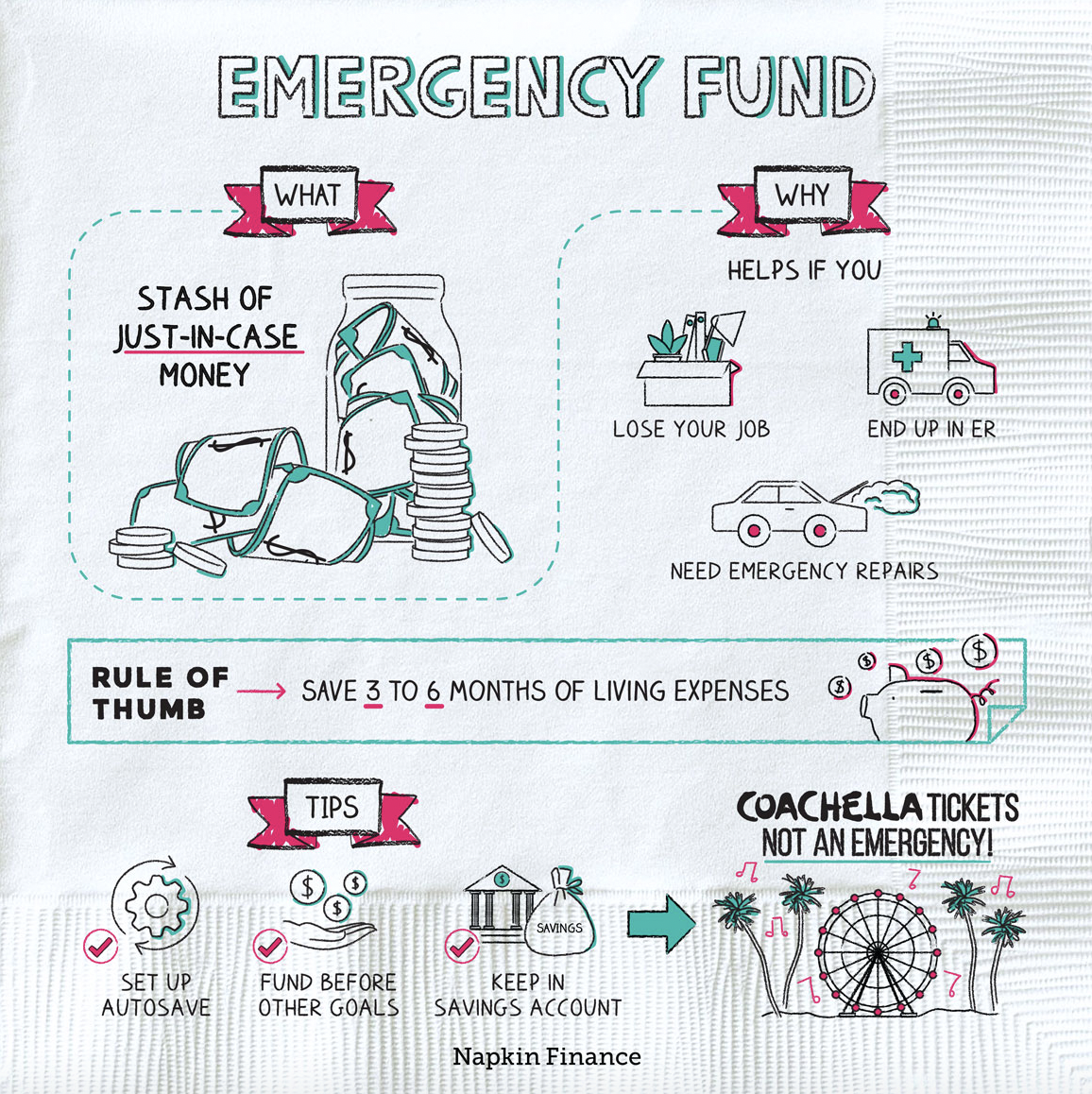

Create an Emergency Fund: Start saving three to six months of living expenses in a high-yield savings account. Here’s a guide to help you get started.

Source: Napkin Finance

🔗 Looking Ahead: Investing Wisely for The Future

Your paycheck is about more than just getting your bills paid, it’s important to also use it to help achieve your financial goals and invest in your future. NOYACK’s Millennial Money Wealth Survey found that nearly 4 out of 10 workers are not currently contributing to their company-based 401(k) or savings accounts.

Taking advantage of any and all benefits your employer offers is a great way to start making steps in the right direction. Here are a few things to keep in mind that can help:

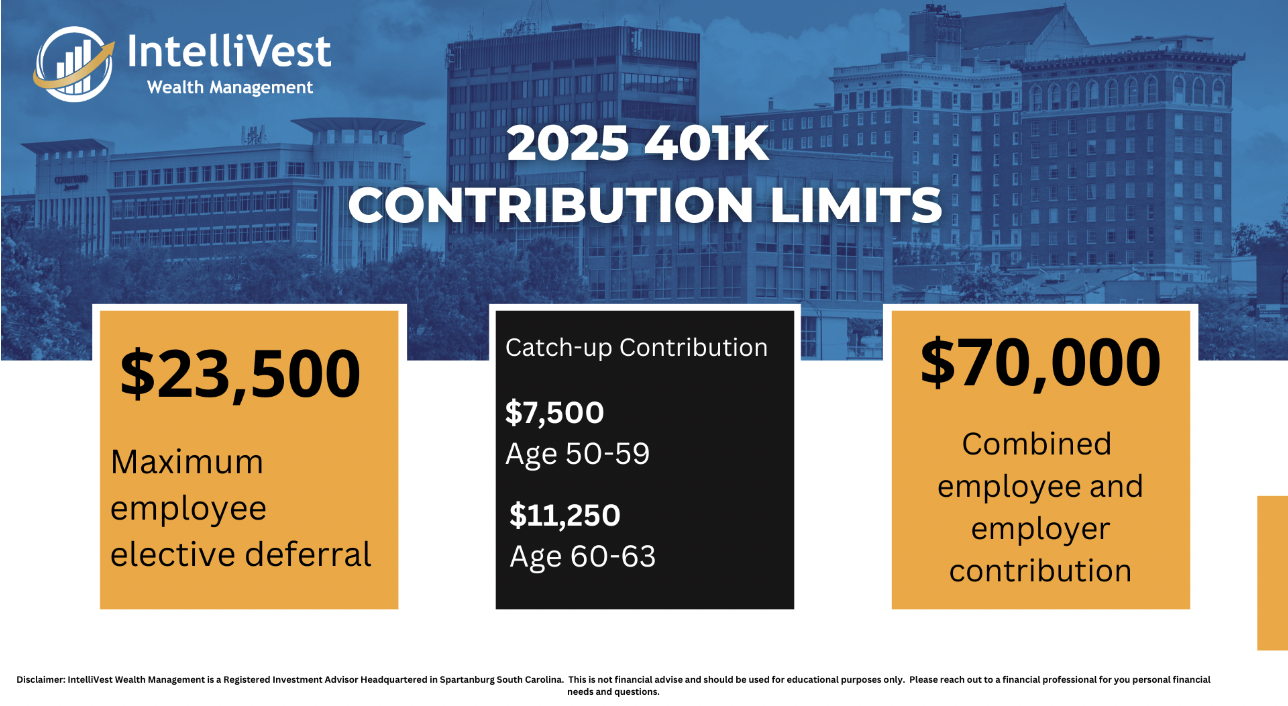

Maximize Employer-Sponsored Retirement Plans: Understand what the contribution limits are annually, and make sure to take advantage of any employer matching available. If your company offers a 100% match on the first 5%, it’s most effective to contribute at least that 5% (otherwise, it’s like giving away free money - and who likes to do that?).

Source: IntelliVest

Utilize Additional Insurance Benefits: Oftentimes employers are able to offer insurance options, like life insurance, disaster insurance, or even disability insurance - at a cheaper rate than you’d be able to obtain on your own.

Consider Employer Stock Purchase Plans (ESPPs): If your company offers a stock purchasing option, it can be a great way to obtain stock at a discounted price.

Consider HSA & FSAs: Health Savings Accounts and Flexible Spending Accounts can be great ways to save money on healthcare costs. Both allow you to use pre-tax/tax-deductible earnings to contribute to healthcare costs for yourself and your family.

✅ The Bottom Line

While it can seem overwhelming at first, the more you familiarize yourself with your paycheck and the different investment opportunities available to you, the more confident you’ll become in your finances.

At Noyack Wealth Club, we provide financial education to 21-45 year olds helping them identify and achieve their financial goals instead of focusing on conspicuous consumption. Whether you’re trying to pay off debt, planning for retirement, or just looking to make the best use of your earnings - our team can help.