CJ Follini, Publisher

Good Morning, NOYACK Fam! 🎄 Happy Sunday before Christmas! 🧑🎄

This holiday season, unwrap financial freedom. ❄️ Tackle student loans now to gift your future self. Grab your mulled wine ( I hate egg nog! ) and dive into smart strategies to save and crush debt. ✨

For many, a college degree unlocks higher salaries—but often at the cost of $40,000 to $65,000 in student loans, delaying milestones like marriage, homeownership, and retirement. Let’s change that with these steps.

Step 1: Understand Your Loan Type

Before tackling your loans, it’s important to identify what kind you have:

Federal Loans: Offer benefits like income-driven repayment (IDR) plans, forgiveness programs, and fixed interest rates.

Private Loans: Typically have higher interest rates and shorter terms but may be refinanced for better conditions.

This distinction lays the foundation for choosing the right strategy.

Step 2: Federal Loan Repayment Options

Federal loans offer multiple repayment plans to suit your financial needs:

Standard Repayment Plan

Fixed payments over 10 years.

Ideal for minimizing interest and paying off debt quickly.

Graduated Repayment Plan

Start with lower payments that increase every two years.

Best for those with rising income potential.

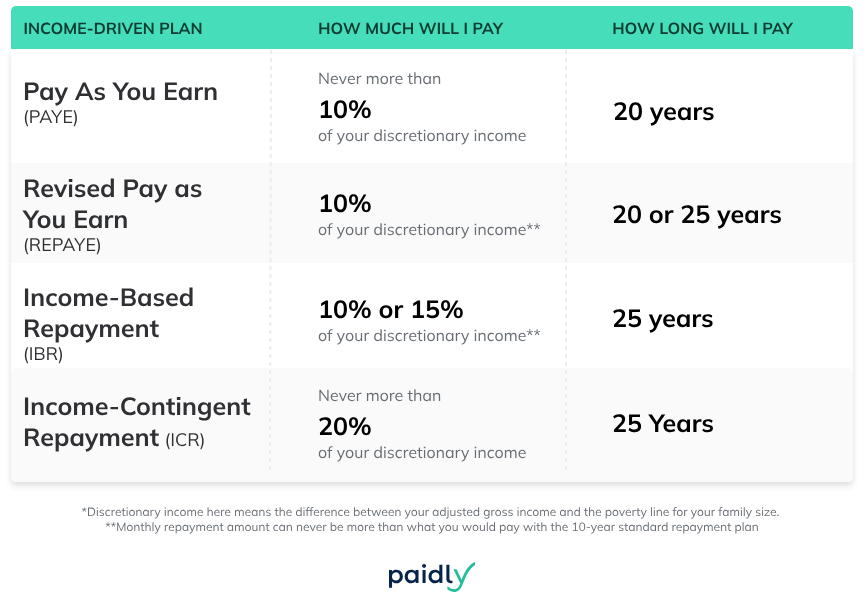

Income-Driven Repayment (IDR) Plans

Payments based on income, capped at 10–20% of discretionary income.

Remaining balance may be forgiven after 20–25 years (though it could be taxable).

Image Source: Paidly

Pro Tip: If you work in public service or a nonprofit, explore Public Service Loan Forgiveness (PSLF), which forgives the balance after 10 years of qualifying payments.

Step 3: Consolidation Loans

For borrowers with multiple federal loans, consolidation can simplify repayment:

Combine loans into one for easier management.

Extend repayment terms up to 30 years to lower monthly payments, though this increases total interest costs.

No application fee for Direct Consolidation Loans.

Step 4: Refinancing Private Loans

Refinancing can be a game-changer, especially for private loans. Benefits of Refinancing:

Lower Interest Rates: Save thousands over the life of the loan.

Streamlined Payments: Combine loans into one monthly payment.

Customizable Terms: Adjust the repayment period to fit your budget and goals.

Refinancing Resources we like:

Lender Name | Bonus Offer | APR Ranges | Visit Link |

|---|---|---|---|

SoFi® | $500 Bonus for refinancing $100k or more (bonus from Student Loan Planner®, not SoFi®) | Fixed: 4.49% - 9.99% APR with all discounts | |

Earnest | $1,000 Bonus for $100k or more | Fixed: 4.29% - 9.74% APR | |

Splash | $1,000 Bonus for $100k or more | Fixed: 4.99% - 10.24% APR | |

Laurel Road | $1,050 Bonus for $100k+ | Fixed: 4.99% - 8.90% APR | |

ELFI | $1,275 Bonus for $150k+ | Fixed: 4.88% - 8.44% APR | |

Credible | $1,250 Bonus for $100k+ | Fixed: 3.85% - 12.10% APR |

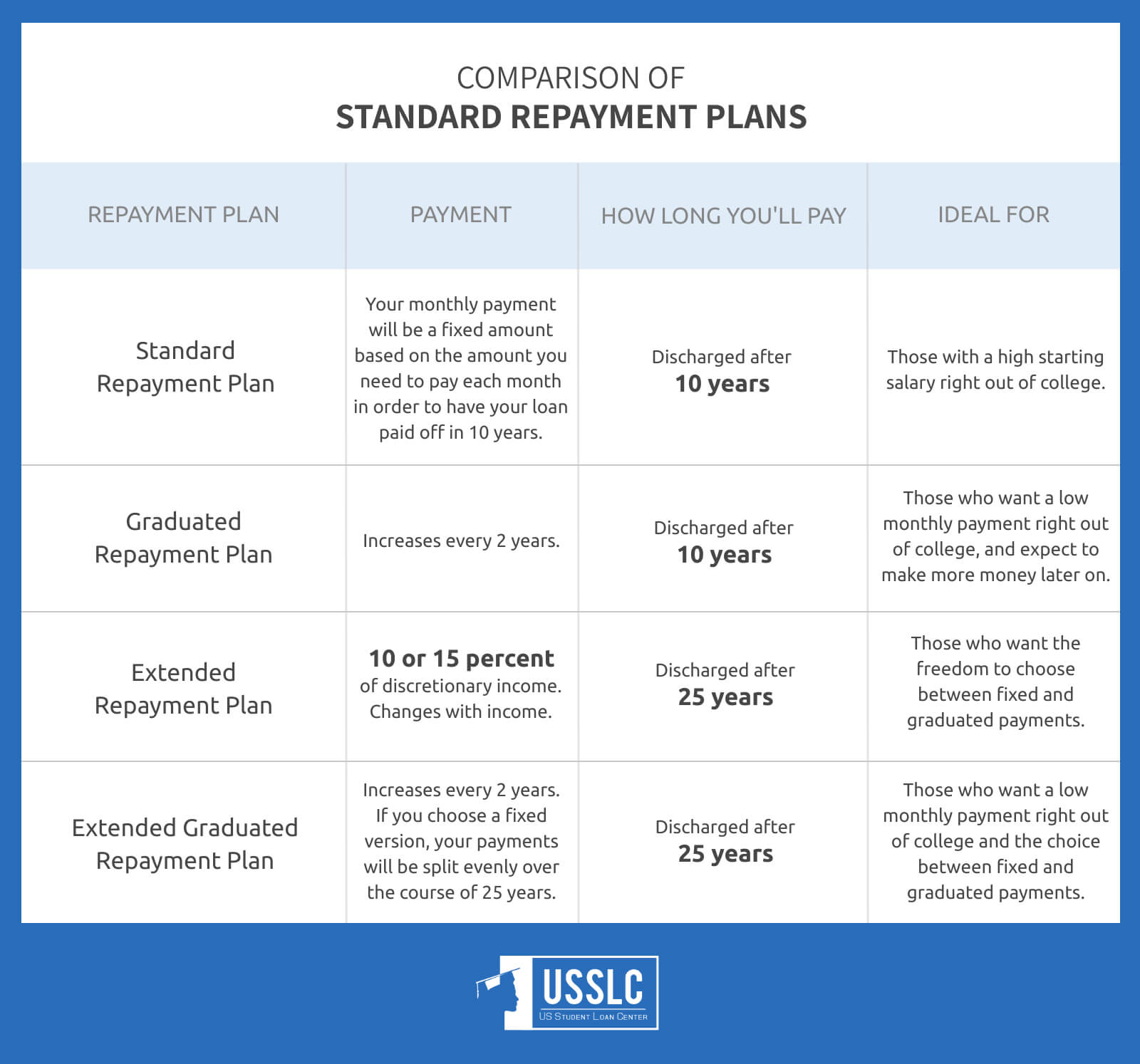

Step 5: Common Pitfalls to Avoid When Refinancing

Refinancing can be powerful, but watch out for these missteps:

Extending Loan Terms Unnecessarily: Longer terms may lower monthly payments but increase total interest.

Overlooking Employer Benefits: Check if your employer offers student loan repayment contributions before refinancing; switching to private loans may disqualify you.

Skipping Comparisons: Always compare rates and terms across lenders to get the best deal.

Losing Federal Protections: Refinancing federal loans into private ones means losing access to IDR plans, forgiveness programs, and deferment options.

Image Source: USSLC

Step 6: Real-Life Inspiration—Sarah’s Story

Sara, a 32-year-old marketing manager, had $60,000 in private student loans with an 8.5% interest rate. Her $735 monthly payments left little room for savings.

Her Refinancing Strategy:

She refinanced at a 4.3% fixed rate with a 10-year term, reducing her monthly payment to $617 and saving $118 monthly.

The Outcome:

Sarah saved over $14,000 in interest and redirected her savings toward buying her first home.

Though her credit score dipped slightly from the hard inquiry, consistent payments improved her score over time.

Sarah’s journey shows how strategic refinancing can lead to financial freedom.

Step 7: Loan Forgiveness Programs

If refinancing isn’t right, consider federal forgiveness programs:

Public Service Loan Forgiveness (PSLF)

PSLF is designed for borrowers working in public service sectors. Key points include:

Eligibility: Full-time employment with a qualifying employer (government organizations, non-profits, or specific not-for-profit organizations)

Requirements: 120 qualifying monthly payments under an income-driven repayment plan

Benefit: Remaining loan balance forgiven tax-free after meeting requirements

Alignment with IDR: PSLF works well with income-driven repayment plans, making payments more manageable during the qualification period

Teacher Loan Forgiveness

This program aims to support educators working in low-income areas:

Eligibility: Full-time teaching for five consecutive years in a qualifying low-income school or educational service agency

Benefit: Up to $17,500 forgiven on Direct Subsidized and Unsubsidized Loans and Subsidized and Unsubsidized Federal Stafford Loans

Amount varies based on subject taught: $17,500 for highly qualified math, science, or special education teachers; $5,000 for other subjects

Cannot be combined with PSLF for the same period of teaching service

Both programs emphasize consistent employment in specific sectors while making regular loan payments. They highlight how strategic career choices can significantly reduce long-term student loan burdens.

Step 8: Stay Ahead with Smart Strategies

Automate Payments: Avoid late fees and possibly lower your interest rate.

Biweekly Payments: Splitting your monthly payment into biweekly installments can reduce interest and shorten the loan term.

Track Your Progress: Apps like Mint or YNAB can help keep your repayment on track.

Budget Wisely: Treat loan payments as a fixed expense in your monthly plan.

This Week’s Expert Interview

As we explored various Student Loan tips and strategies, we sat down with Nate Hoskin, founder of Hoskin Capital, and a financial planner with vast experience overcoming student loan debt. Check out our Podcast with Nate below 👇 as we dig deeper into the topic and gain some great insights first hand from Nate: