CJ Follini, Publisher

Good morning, Noyackers!

Student loans are one of the most significant financial commitments many people face. The right strategy could save you thousands over time, while the wrong one could cost you money, time, and financial flexibility. The choice between refinancing for a lower interest rate and pursuing loan forgiveness depends on your career path, income, and long-term financial goals.

This guide will help you break down your options, determine whether forgiveness or refinancing is the right choice for you, and take action on a strategy that aligns with your financial future.

📊 Quick Poll: What’s Your Biggest Student Loan Concern?

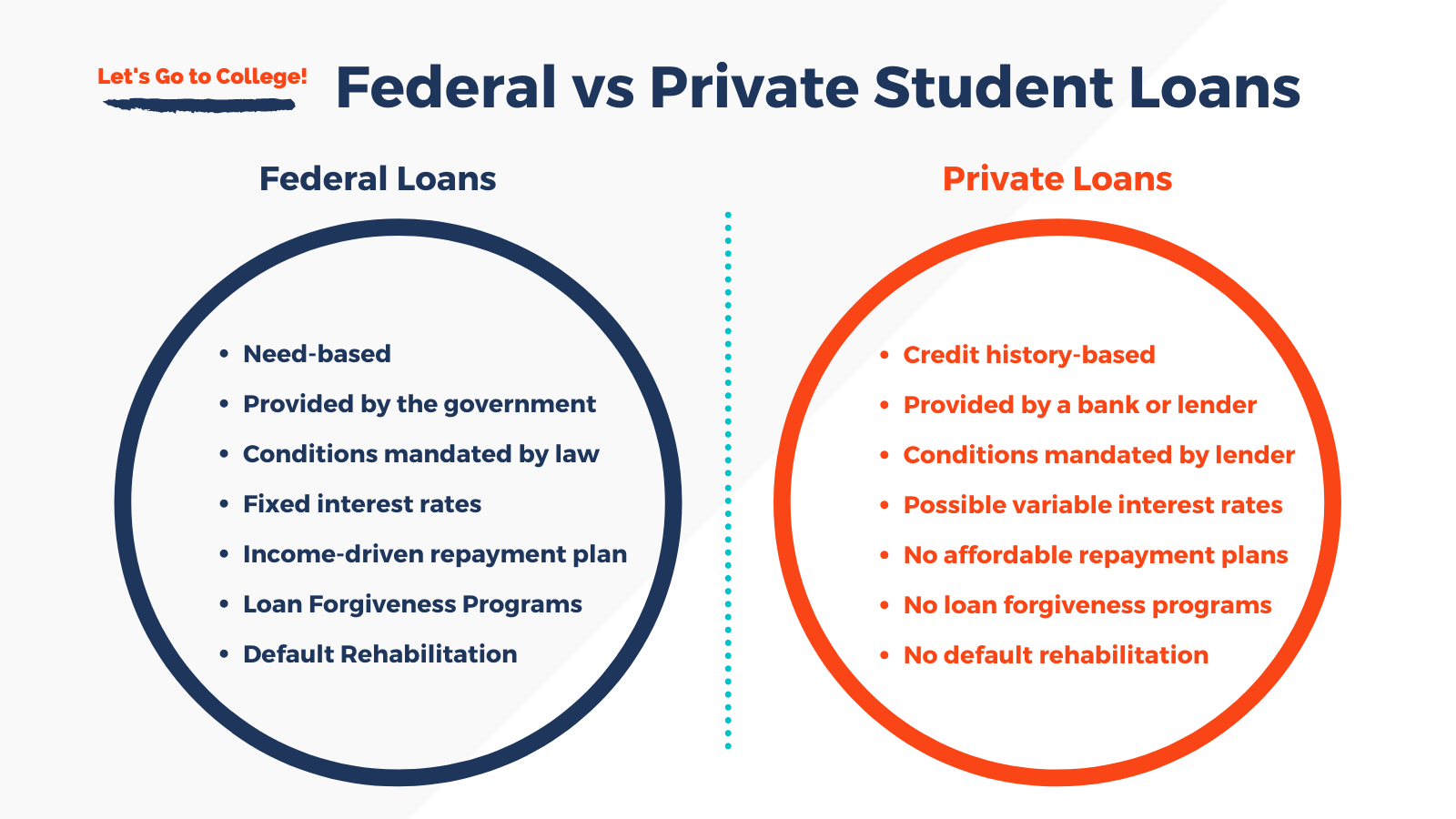

Step 1: Understand What Type of Loans You Have

Before deciding how to tackle your loans, you need to understand what kind of loans you have, because forgiveness is only available for federal loans.

Check Your Loan Type

Federal Loans → Eligible for forgiveness and income-driven repayment (IDR) plans.

Private Loans → Forgiveness isn’t an option, but refinancing may help lower your interest rate.

Quick Action Step:

📌 Log into Studentaid.gov to confirm if your loans are federal or private.

Source: Let's Go to College CA

Step 2: Should You Choose Loan Forgiveness?

If you have federal student loans, you may qualify for forgiveness programs that could eliminate your debt after a certain number of payments. Let’s break down the key programs.

Public Service Loan Forgiveness (PSLF) – Best for Government & Nonprofit Workers

Who qualifies?

Employees of government agencies, nonprofits, or qualifying public service organizations (teachers, healthcare professionals, social workers, military, etc.).

How it works:

Remaining loan balance is forgiven after 120 qualifying payments (about 10 years).

Must be on an income-driven repayment (IDR) plan.

⚠ Warning: If you switch jobs before hitting 120 payments, you lose PSLF eligibility.

Income-Driven Repayment (IDR) Forgiveness – A Long-Term Strategy

Who qualifies?

Any borrower with federal loans enrolled in an IDR plan (IBR, PAYE, REPAYE, SAVE).

How it works:

Monthly payments capped at 10-20% of discretionary income.

Remaining balance forgiven after 20-25 years.

⚠ Heads-up: Unlike PSLF, forgiven balances may be taxed as income when forgiven.

Source: Highway Benefits

Teacher Loan Forgiveness – A Faster Forgiveness Path

Who qualifies?

Teachers who work at least five years in a low-income school or district.

How it works:

Forgives up to $17,500 of federal student loans after five years.

Cannot be combined with PSLF for the same period of service.

Additional Federal Forgiveness Programs:

Borrower Defense to Repayment: If you were misled by your school.

Total & Permanent Disability Discharge: If you become permanently disabled.

Military & AmeriCorps Forgiveness: For service-related repayment benefits.

Check your PSLF eligibility here: PSLF Help Tool

Step 3: Should You Refinance Instead?

If you have private loans or high-interest federal loans, refinancing may help you save money by securing a lower interest rate or better repayment terms.

Who Should Refinance?

✔ You have private loans with a high interest rate.

✔ You have a good credit score (650+) and stable income.

✔ You want to lower your monthly payments or shorten your loan term.

Who Should NOT Refinance?

❌ If you might qualify for PSLF or IDR forgiveness.

❌ If you want to keep federal protections like forbearance and deferment.

❌ If your income is unstable and you need repayment flexibility.

What Happens If You Refinance Federal Loans?

🚨 You lose all federal benefits:

No access to PSLF, IDR, or deferment.

No government relief programs if new policies are introduced.

"What If" Scenario:

What if I refinance and then lose my job?

→ Unlike federal loans, private loans don’t offer income-based repayment or forbearance options. Make sure you have an emergency fund before refinancing!

Compare refinance lenders here: Credible Student Loan Comparison

Still not sure? Ask yourself these questions:

Do you work in public service or a nonprofit? → Forgiveness is likely the better path.

Is your income high and stable? → Refinancing could save you thousands.

Do you need flexibility in case of hardship? → Stick with federal repayment options.

Take Action Today

If you’re considering loan forgiveness:

Check if your employer qualifies for PSLF 👉 PSLF Tool

Apply for an Income-Driven Repayment Plan 👉 IDR Application

If you’re considering refinancing:

Compare lenders for the best rate 👉 Compare Here

Prequalify without affecting your credit 👉 Earnest Refinance Calculator

Still undecided? Reply and tell us your situation! We’re here to help.

Final Thoughts

There’s no one-size-fits-all solution for student loan repayment. The best approach depends on your career, income potential, and financial goals.

If you qualify for forgiveness, take advantage of it. If refinancing saves you money, it may be the better move. But whatever you do—don’t ignore your options.

💡 Need more insights? Follow our community at Noyack Wealth Club.

Let’s take control of student debt—one smart decision at a time.