Est. Reading Time: 5 min

Table of Contents

For younger investors, housing decisions can have a huge impact on your wealth journey. Here’s a story and a lesson I learned about renting vs. owning when I was young which is over four presidents ago. My friend Doug Levine, Founder of Crunch Fitness, gave me great advice.

At the time he was renting and he could certainly afford a house, in fact he could afford a really expensive one so I asked him why was he still renting? Because growing up with immigrant parents from Italy, homeownership was the embodiment of the dream. Doug said that if I had any nterest in considering a home as an investment, then i needed to make decisions to own or sell opposite of the crowd. Doug sold his house at the top of a housing cycle in 1989, made a significant profit, and rented until the housing cycle crashed and had a first bottom in 1993. Thats when he pounced and bought a fantastic home at 40% less than it cost at the peak.

Zig when people zag, zag when people zig is the lesson I learned from Doug Levine.

Everyone knows that housing costs can make up a big chunk of your monthly expenses. But deciding whether to rent or buy can also have knock-on effects for your entire financial life, from asset allocation to employment flexibility.

Historically, homeownership has been held up as an important milestone for young adults (June is even celebrated as National Homeownership Month). But just because homeownership has cultural cachet doesn’t mean it’s always the best financial move.

Today, we’re going to take a look at the rent vs. own debate, exploring why:

Comparing renting to owning is usually like comparing apples and oranges,

The investment case for homeownership isn’t as strong as you might think,

And the four questions that can help you decide whether to rent or own.

It’s really hard to compare renting and owning

There’s one big reason why it’s so hard to find a simple answer to the rent vs. own question – it’s almost impossible to compare the two options on a fair basis.

To understand what I mean by that, let’s take a look at Bankrate’s most recent study exploring the rent vs. own dynamic. Published just a few months ago, Bankrate found:

Renting is currently cheaper nationwide. The typical monthly mortgage payment of a median-priced home in the US is $2,703, compared with a typical monthly rent of $1,979.

Renting is cheaper than owning in all of the top 50 US metro areas, with the biggest differences seen in San Francisco, San Jose, and Seattle.

In 21 US metro areas, the monthly cost of owning is at least 50% higher than renting.

Great, we have an answer – renting is cheaper… right?

Not quite. There’s a big problem with this comparison, and it’s not what you might expect.

You probably already know that mortgage payments build equity, while rental payments do not. In other words, a portion of every mortgage payment is an investment. Unlike rental payments, mortgage payments aren’t entirely an expense, so it’s not fair to compare them on an equivalent basis.

But an even bigger issue is that Bankrate didn’t compare renting and owning the same home! They looked at payments on the typical rented unit and the typical owned unit nationwide – and the “typical” unit looks wildly different in each case.

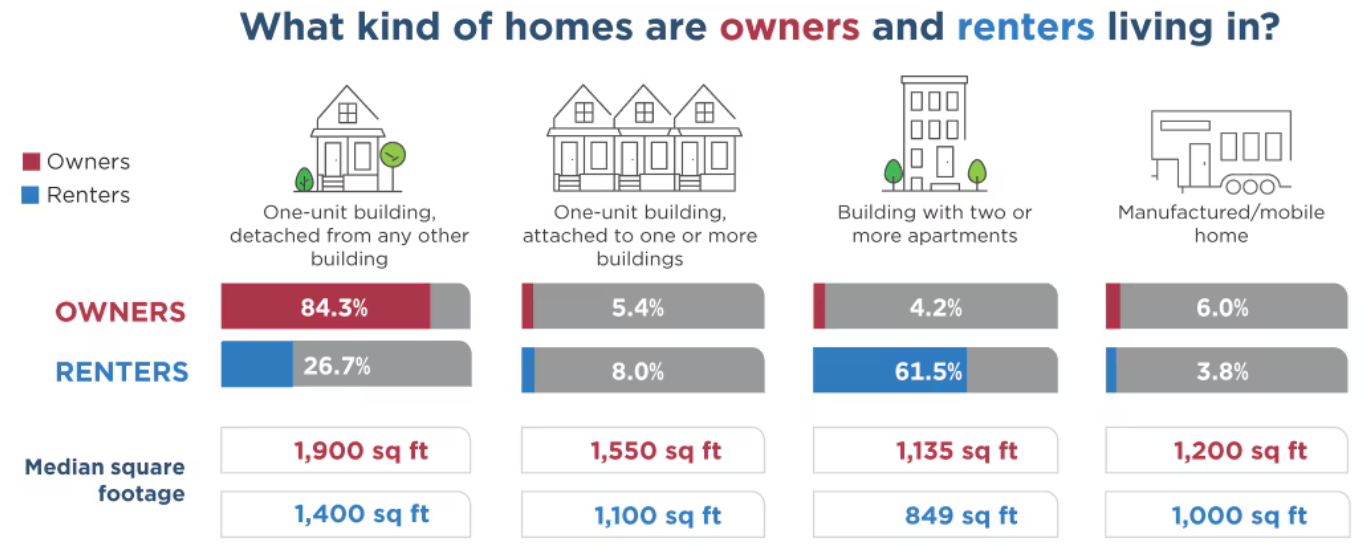

According to the most recent Profile of Owners and Renters from the US Census, 84.3% of homeowners live in a single or multifamily home, while 61.5% of renters live in an apartment building.

And if you run the numbers, you’ll find that owners have median square footage 76.6% higher than renters – so is it really any surprise that renting is so much cheaper on average?

Another problem with trying to come up with a clear answer here is that the affordability of both options is constantly changing. Right now, the ratio of home prices to average incomes is at one of its highest levels in history, meaning homeownership might not be feasible.

But this is a figure that tends to fluctuate with market cycles, so the right answer today isn’t necessarily the right answer tomorrow.

The investment case for homeownership can be misleading

Another reason that the rent vs. own comparison can be deceptively complicated? The investment case for homeownership isn’t as strong as you’d think.

In the last section, we mentioned that a portion of every mortgage payment is an investment since it goes toward your home equity (this portion increases over time, with the bulk of early payments going to interest). In comparison, renting is often seen as “throwing money away,” since you’re not building any equity.

Historically, putting money into your home hasn’t been a bad investment. The value of American homes has climbed markedly over the past four decades. Despite a few crisis-related blips, the Case-Shiller index, which measures national home prices, has seen annualized returns of roughly 5% since 2000.

Don’t forget about that lucrative capital gains tax exclusion from selling your home…

So, why am I saying that the investment case for homeownership can be overstated? Because people frequently ignore the opportunity cost of investing the cash you save by renting.

The Bankrate study showed that if you opt for renting your monthly housing payments are almost $700 lower. That’s $700 you can funnel right into high-return investments, including alternatives like fine art and private equity.

And if you’re a renter who’s still interested in getting exposure to the real estate market, there are plenty of places you can put that excess cash – including, by the way, our very own Noyack Logistics Income REIT.

Whether homeownership or rent + invest is ultimately a better wealth-building path depends on a tremendous number of factors, including home appreciation rates in your area, the asset allocation of your portfolio, and how disciplined you are about saving & investing.

The bottom line, though, is that we can’t write off renting as throwing away money – and we can’t naively assume homeownership is always a better investment strategy.

This is a lifestyle decision, not just a financial decision

There are a few calculators out there that can help you crunch the rent vs. own numbers, including The New York Times (subscribers only) and NerdWallet.

But ultimately, this is much more than a financial decision. It’s rare that you’ll have to consider renting or owning the exact same property. Instead, you’ll usually be deciding between two different units – and thus two different lifestyles.

If you’re trying to figure out whether renting or owning makes sense, here are some questions to ask yourself:

Do I prefer certainty or flexibility?

If you buy a home with a fixed-price mortgage, you gain the certainty of knowing exactly where you’ll be living and what you’ll be paying for a decade or more. If you want to move, though, you’ll have to incur some expensive one-off costs. In comparison, renting allows for more moving flexibility, but at the expense of potential cost increases each year.

Do I want to be responsible for emergencies?

If you’re renting and a pipe bursts, your landlord has to foot the bill to fix it (they might even have to pay to put you up in a hotel for a night or two). If you’re a homeowner, though, costs for emergency repairs fall on your shoulders.

Am I disciplined enough to save on my own?

We mentioned that the opportunity cost of the cash saved by renting makes it a competitive wealth-building option. But that’s only true if you’re willing to actually save and invest the excess cash. A mortgage, on the other hand, is like a forced savings program.

Am I willing to invest in a community?

Homeownership requires a greater commitment to being an active and productive member of your local community – and not just because you’re likely to stick around in that community for longer. Your property value is tied to the character, values, and livability of the area you call home, so putting down roots and investing in the community goes hand in hand with homeownership.

POLL OF THE WEEK

Do you currently rent or own – and which one would you prefer?

📺 WHAT WE'RE WATCHING

Unfortunately, homeownership is an increasingly out-of-reach option for younger Americans. This CNBC segment explores the tough state of the US housing market for first-time homebuyers.

👂 WHAT WE’RE LISTENING TO

This podcast from research firm Morningstar explores how home equity can be used for retirement planning, with two experts weighing in on the value of tools like reverse mortgages.

📖 WHAT WE’RE READING

This Zillow study explores the rent vs. own question in depth, using mathematical modeling and scenario stress-testing to decide which is better (spoiler alert: it depends).

Deals & Discounts 4 You From Us

Make your estate plan count | 20% Discount Code for NWW subscribers only!

Puzzle of The Week

Refer A Friend Refer A Friend Refer A Friend Refer A Friend Refer A Friend Refer A Friend … And Win Prizes!